Our report covers trends in 14 categories (AI Infrastructure, App & Software Development, Crypto, Data analytics, EdTech, Enterprise, ESG, Fintech, Health / Bio Tech, Industries, Legal, Media & Advertisement, Science & Research, Services & Retail) and database of startups backed by leading 13 venture capital firms (a16z - Andreessen Horowitz, Sequoia Capita, YC - YCombinator, Index Ventures, Founders Fund, Bessemer Venture Partners, Insight Partners, Accel, Lightspeed Venture Partners, General Catalyst, New Enterprise Associates (NEA), Tiger Global Management, SV Angel).

Our monthly September report is dedicated to the analysis of current trends in venture financing. We analyze the activities of the largest and most experienced firms — which technologies and sectors they support, and what investments they are making. Current venture investments demonstrate how the largest companies view the venture market now and forecast the development of venture capital and technology in the future.

We believe that our analysis will help venture investors and startup founders better understand how leading companies view the current and future development of venture finance and technology.

In September we analyzed the rounds of 5 most famous and most influential venture investors:

- Andreessen Horowitz (a16z)

- General Catalyst

- Sequoia Capital

- Lightspeed Venture Partners

- Y Combinator

Our September our database includes 116 deals concluded/announced with the participation of these companies in September 2025—approximately 5% of the total number of venture investments for September. However, if measured by unicorns, these companies are the absolute market leaders: in September, 11 companies supported by these firms became Unicorns.

For this research we've excluded so-called 'Mega Rounds'—multibillion-dollar deals (like those with OpenAI and xAI) that involve institutional investors. The report also excludes startups developing defense projects, as the success of these startups does not depend on market factors.

Sources: Crunchbase open data, PitchBook open data, Websites of selected venture investors and startups, articles of leading mass media, CDP Center database and calculations.

KEY INDICATORS: 2024 - 9.2025

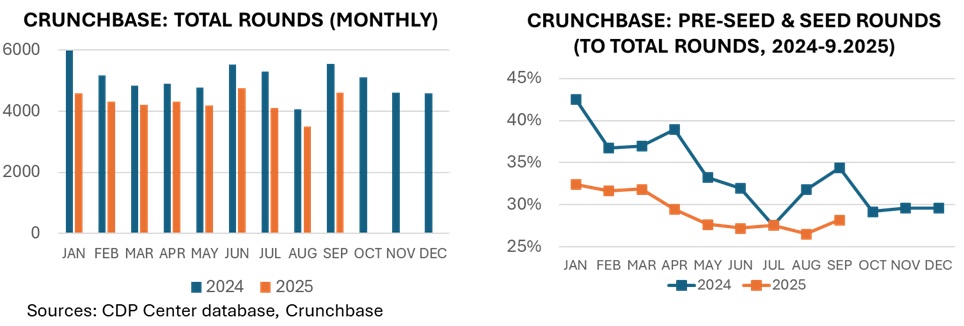

Overall, as of October 4, 2025 (according to Crunchbase and DealRoom data for the first nine months of 2025), we observe that the number of funding rounds in 2025 has been lower each month than in 2024 (down by an average of -16.7% across all months). In September 2025, according to our calculations (Crunchbase data & CDP calculations), there were 4,596 rounds compared to 5,539 in September 2024 (a -17%* decrease).

Our analysis of Crunchbase data shows that over the past months, the share of Pre-Seed Rounds / Incubator Stage and Seed Rounds has also decreased significantly, falling from an average of 35% to 29% of the total number of rounds over the nine months (September 2025 saw 28%).

We attribute this to the significant rise in the popularity of AI-focused startups, which has led to higher requirements for the IT competencies of startup teams.

The second factor is: with the Fed's interest rates remaining high, the total amount of venture funding on the market is strained. According to our calculations, a one percentage point drop in the Fed's rate leads to $9.6 billion in annual venture investment growth in the U.S. market.

Notes:

* The deal count may slightly increase in the coming months; however, the downward trend in the number of deals is a sustained one, according to data from Crunchbase and Dealroom, as well as the joint report by NVCA & Pitchbook.

** For this research we've excluded so-called "Mega Rounds"—multibillion-dollar deals (like those with OpenAI , xAI , Mistral AI) that involve institutional investors—from our research.

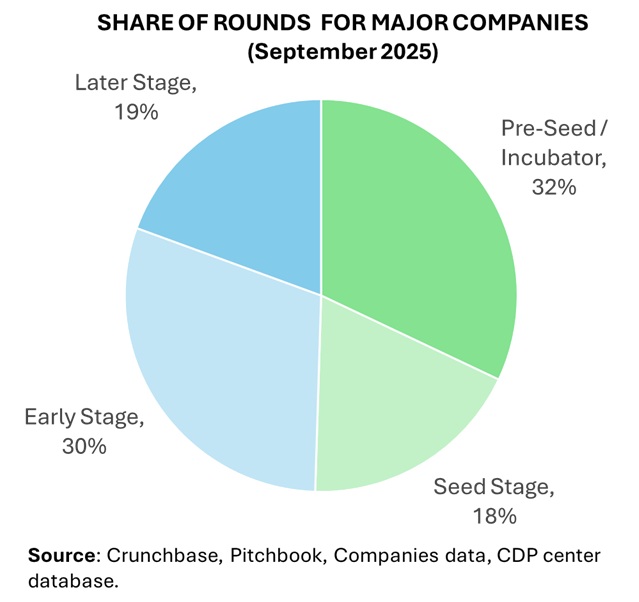

INVESTMENTS BY ROUNDS STAGE

In September, the top venture funds backed 32% Pre-Seed / Incubator stage rounds, 18% on Seed Stage.

The most share of Pre-Seed / Incubator, Seed rounds backed by VC major companies are in Media & Advertising – 89%.

Enterprises Pre-Seed / Incubator, Seed Rounds backed by VC major companies reached – 55%.

The share of startups that have implemented or are implementing AI solutions (among the largest venture funds) at the Incubator/Pre-Seed/Seed stage reaches 82%.

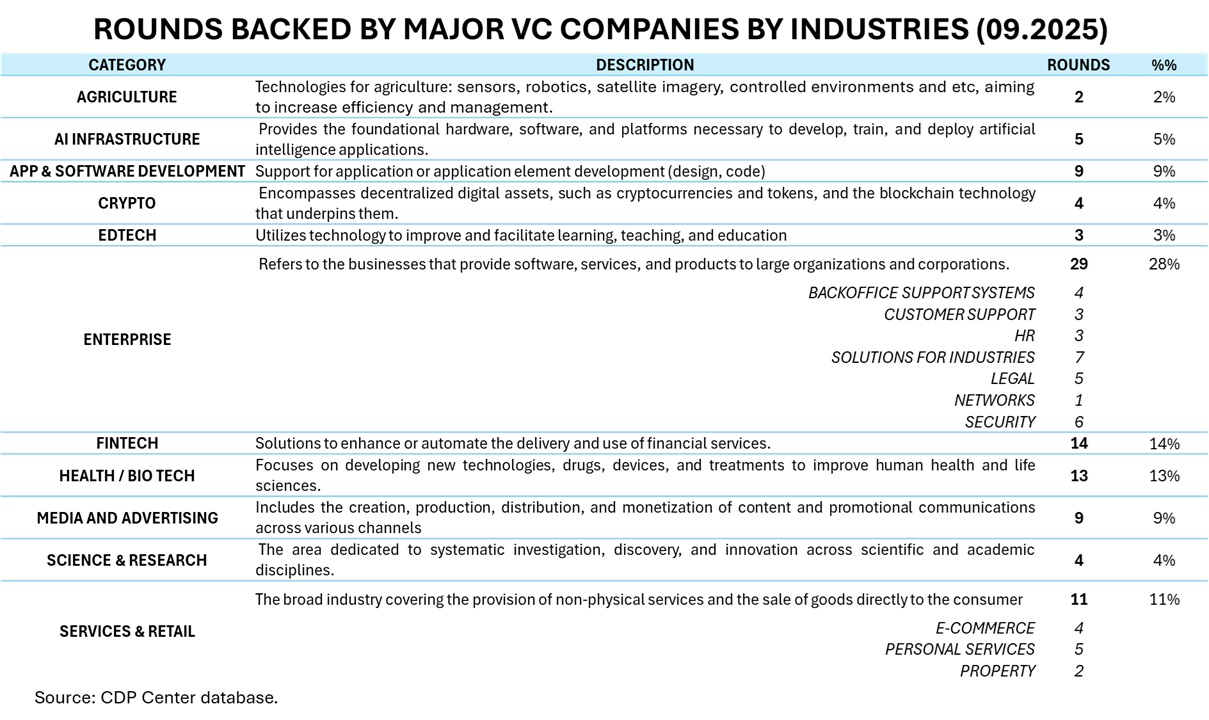

ROUNDS BACKED BY MAJOR VC COMPANIES BY INDUSTRIES (09.2025)

In September, 70% of startups supported by leading firms directly indicated in various places that their product is an AI model/agent or contains AI elements. Interestingly, many leading startups in developed stages are already changing their products by adding new AI capabilities.

Among the industries, we particularly highlight the core of AI - AI Infrastructure - 5 startups that create the infrastructure for implementing the projects of others.

Among the most AI-saturated industries are:

- App & Software Development (9 startups) - support for code writing and complex application development.

- Enterprise: Backoffice Support Systems (5 startups) - focused on introducing artificial intelligence into the routine operations of companies.

- Enterprise: Customer Support (3 startups) - enterprise customer support for companies.

- Enterprise: HR (3 startups) - replacement of routine HR tasks.

- Science & Research (4 startups) - support for technological research and complex developments.

Also of interest are the Enterprise Backoffice Support Systems (5 startups), which are aimed at introducing AI to assist in carrying out company functions.

The penetration of AI is also extremely high in sectors such as Media & Advertising (comprehensive generation of video, images, as well as advertising campaign analytics), and Enterprise: Security and Customers: Personal Services.

ROUNDS BACKED BY MAJOR VC COMPANIES BY INDUSTRIES (09.2025)

AI INFRASTRUCTURE

In September, 5 funding rounds were directed towards projects that support the development and applied use of artificial intelligence applications. We found the startup Paid (Light Speed), which creates infrastructure for billing and cost tracking for AI agents, particularly interesting.

One of the two unicorns, Modular (General Catalyst), is also of special interest, as it offers a cloud platform for building, optimizing, and scaling AI systems.

APP & SOFTWARE DEVELOPMENT

In September, 9 startup projects were supported, all aimed at simplifying application development, including writing and correcting code, and developing design. All the startups supported by leading firms offer solutions that leverage the benefits of artificial intelligence.

The new startup Specific (Y Combinator) promises to develop an AI capable of creating complete applications using only textual descriptions. PostHog (Y Combinator), which achieved unicorn status, introduced a complete operating system containing a comprehensive set of tools for developers.

ENTERPRISE

This sector is the most focused on applied solutions for corporate clients. In September 2025, 29 projects (28% of the total) were supported.

All 4 Backoffice Support Systems projects, aimed at replacing routine tasks and workflows, supported by leading venture investors, belong to the Pre-Seed / Incubator rounds.

All 3 projects in the Customer Support sector are focused on facilitating customer interaction using AI. One of the startups, Quo (General Catalyst), which received a funding round of over USD 100 million in September 2025, offers a single platform to gather all company communications (calls, messages, emails).

3 startups in the HR sector were supported, all of which are implementing AI in human resources management. DianaHR (General Catalyst) offers AI-powered HR tools for main HR functions, including onboarding, attendance, payroll, and employee management. Also of interest is AlexAI (Y Combinator), which is focused on supporting AI-based recruiting, with specialization in the interview process: phone screens, video interviews, fraud detection, etc. Jucibox is aimed at a proactive task: to search, engage, and manage potential hires (Agent for Talent search).

In general, Legal tasks are aimed at automating the routine tasks of legal departments. Legora (General Catalyst) became a new unicorn, offering AI support for document review, drafting, editing, research, and workflows.

The Enterprise: Security sector was quite active in September 2025, with leading venture investors supporting 6 projects, 5 of which are aimed at involving AI in prevention, monitoring, and protection of companies against risks and threats.

FINTECH

This sector is traditionally a key area for venture capital. 9 out of 15 projects are implementing AI tools for the use of financial instruments, simplification of financial analysis, and support for corporate financial functions.

We found startup Mainflow particularly interesting, as they attempt to rethink the approach to providing data and opportunities for private investors, creating a flexible and app for investing and finance management (Y Combinator).

HEALTH / BIO TECH

This sector has reoriented itself towards using artificial intelligence in research, development, and systems supporting the work of medical institutions. We specifically highlight startups that are integrating AI into doctors' practices: Doctronic (LightSpeed) offers a solution that embeds AI as an element of medical care. The startup proposes initial interaction with artificial intelligence, followed by a meeting with a licensed physician.

Two startups, Judi Health (backed by General Catalyst) and Thyme Care (a16z), have reached Unicorn status.

MEDIA AND ADVERTISING

This is the most effervescent sector for new projects. Out of 9 projects, 8 use AI to generate complex and meaningful videos, or are used for analyzing and improving search results, and supporting and analyzing the results of marketing campaigns.

We highlight the service Koyal (Y Combinator), which presented the first project for generating multi-element videos from a user's audio recording. The project supports the creation of a user avatar.

SCIENCE & RESEARCH

All 4 startups in this category used AI to support research and development, ranging from regular scientific activity to solving specific industry-related problems. This includes two startups: Lila Sciences (AI for hardest problems with probability approximation reasoning, General Catalyst) and AA-I Technologies (AI for chemistry, material and life sciences, Light Speed).

SERVICES & RETAIL

Among the leading venture investors, 11 venture investments were allocated to this sector.

Among the most interesting in the Personal Services sector—that is, startups creating services for personal consumption. Interestingly, all 5 Personal Services startups contain AI elements. Two of the startups are designed to assist with calendar management and personal correspondence. We find the new startup Sorce (AI for job seekers, Y Combinator) and the solutions from Enter for resolving common simple legal disputes (Brazil, Y Combinator) to be the most compelling.

If you are interested in information about venture industry insights and current funding trends, subscribe to our monthly reports here: venture.cdp.center

Each report covers trends in 14 categories (AI Infrastructure, App & Software Development, Crypto, Data analytics, EdTech, Enterprise, ESG, Fintech, Health / Bio Tech, Industries, Legal, Media & Advertisement, Science & Research, Services & Retail) and database of startups backed by leading 13 venture capital firms(a16z - Andreessen Horowitz, Sequoia Capita, YC - YCombinator, Index Ventures, Founders Fund, Bessemer Venture Partners, Insight Partners, Accel, Lightspeed Venture Partners, General Catalyst, New Enterprise Associates (NEA), Tiger Global Management, SV Angel)

The detailed data on the company rounds is presented in the full report.

DISCLAIMER: This report analyzes market trends and is not a source of definitive or complete data. Due to the dynamic nature of the market, it's impossible to provide 100% accurate, allencompassing data. Our research is based on the information we have gathered through different public sources, and it may be corrected as new data becomes available. Investing in startups is inherently challenging and carries significant risks. This report should not be construed as investment, tax, or legal advice. We are not making any recommendations. If you are considering starting a business or making venture investments, you should consult with qualified professionals, who can provide personalized and competent advice.

.webp)