In the second part of our tax environment review, we continue our overview of best practices from leading global startup ecosystems for creating a favorable tax environment that supports the growth of startups to scale-up and unicorn levels.

The CDP Center's experts prepared an overview of best practices for creating direct incentives for investors in venture projects. This review specifically presents incentives aimed at reducing the tax burden on Personal Income Tax (PIT) for investors and Capital Gains Tax (CGT).

Of course, for successful venture investing, the focus isn't solely on capital gains. Investors also look closely at incentives that positively impact a company's free cash flow, allow for cheaper development investments, and ultimately improve the company's overall risk-return profile. In our next two issues, we'll dive into these vital incentives—specifically, R&D incentives and job growth incentives—which are critical for high-tech, fast-growing startups.

Currently, even early-stage startups strive to engage with the international venture capital market, attracting funds from more than just their domestic investors. As they grow and scale, working with venture capitalists from different countries becomes vital, especially when expanding for new markets and accelerating innovation.

In turn, when making financial decisions, investors prioritize supporting startups operating in jurisdictions that offer the most attractive risk-return ratio and favorable operating conditions. Capital gains taxation, of course, plays a significant role in their decision-making.

Almost all countries where the leading startup ecosystems are located, offer incentives for venture capitalists and business angels, whether through PIT or CGT.

A review of best practices for creating tax incentives for startups—particularly those in the ICT and AI industries—must naturally begin with the United States.

We will highlight best practices both at the federal level and within the individual states that host the largest startup ecosystems.

At the federal level, the cornerstone incentive is the large-scale Qualified Small Business Stock (QSBS) Incentive. This mechanism was recently enhanced by increasing the company turnover limit and introducing several other innovations, significantly boosting its attractiveness to investors.

Qualified Small Business Stock (QSBS) Incentive.

The Federal QSBS is one of the most significant catalysts for the U.S. venture capital market, as it provides a 100% exemption from the federal capital gains tax rate and the most majority US states conform to the federal QSBS exclusion. This means that capital gains from the sale of eligible stock are also excluded from state income tax. As a result this tax incentive is attractive and beneficial to both U.S. investors and investors from other countries.

The holding period for a full 100% exclusion is generally five years. For stock acquired after July 4, 2025, there are tiered benefits for shorter holding periods (50% exclusion for three years, 75% for four years).

The amount of gain that can be excluded is the greater of:

$15 million (for stock acquired after July 4, 2025; otherwise, it's $10 million)

10 times the adjusted basis of the stock (the original cost of the stock).

The company must be a domestic C corporation, it is a type of business entity in the United States that is treated as a separate legal and tax-paying entity from its owners (shareholders) and it can have an unlimited number of shareholders. Certain businesses in the fields are excluded: health, law, accounting, financial services, and those involving farming, mining, or real estate.

The company's aggregate gross assets must not exceed $75 million (for stock acquired after July 4, 2025; earlier it was $50 million) at any time from its formation until immediately after the stock is issued.

The taxpayer's holding period, at least 80% (by value) of the company's assets must be used in the active conduct of a "qualified trade or business." The stock must be acquired directly from the issuing company in exchange for money, property (other than stock), or as compensation for services.

The taxpayer must be a non-corporate entity, such as an individual, a partnership, or a trust.

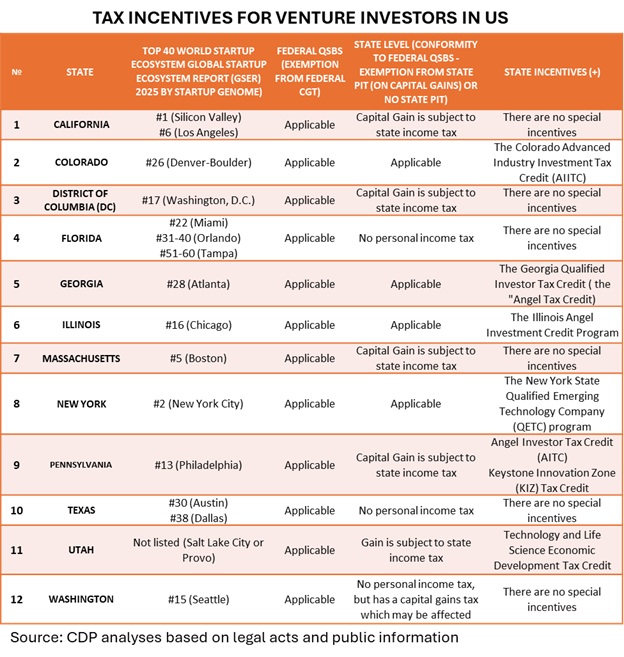

Among the states where the largest startup ecosystems are located, we can distinguish four groups:

The First Group: Zero PIT and Partial QSBS Conformance

States in this group have partially confirmed the Federal QSBS rules but also maintain a zero Personal Income Tax (PIT), which includes no tax on capital gains. This includes Florida (top startup ecosystem: Miami #22, Orlando #31-40, Tampa #51-60) and Texas (top startup ecosystem: Austin #30, Dallas #38). This structure means that investors face no state-level restrictions on incentives, such as limits on company size or the required length of time a company's shares must be held to qualify for state tax benefits.

The Second Group: Full QSBS Conformance with Proprietary Programs

States in this group have fully confirmed the federal incentive and provide state tax incentives in accordance with federal law. They also have their own programs to stimulate investment in startups. This group includes Colorado (Denver-Boulder #26), Georgia (Atlanta #28), Illinois (Chicago #16), and New York (New York City #2).

The following characteristics are common to the additional tax incentives for investors in these states:

• The company must be headquartered in the state, or at least 50% of the company's employees must be employed in the state.

• The programs are aimed at stimulating investment in relatively young companies operating in technology markets for no more than 5 to 10 years, with a focus on those showing significant job-creation potential.

• The programs offer investors a tax credit of 25%−35% of the state's PIT liability. This credit can typically be claimed over multiple tax periods. However, the total credit amount an investor can claim is capped (for instance, the maximum in NY is $350K).

• Some states have established an investment threshold of at least $10,000, along with restrictions on shareholding and holding periods, among other conditions.

The Third Group: Non-Conforming QSBS BUT Company-Focused Incentives

This group has not confirmed the federal tax exemption and levies the state capital gains rate. Crucially, there is no alternative existing program providing direct incentives for startup investors. It is important to note that these states have extensive incentives aimed at providing tax benefits to companies for investing in job creation and innovation: California (Silicon Valley #1, Los Angeles #6), District of Columbia (DC) (Washington, D.C. #17), and Massachusetts (Boston #5). Clearly, these company-focused incentives also increase the attractiveness of investments at different stages of startup development and growth. (We will cover this in more detail in future issues.)

The Fourth Group: Non-Conforming with Alternative Investment Program

This group has not certified the federal incentives but maintains its own separate startup investment incentive program: Pennsylvania (Philadelphia #13).

It is also important to highlight best practices in our review for encouraging investors to invest in startups across European countries. Europe is undoubtedly the second most important financial market in the world, and as the concept of a single European financial market is implemented, its position will only strengthen.

In the full report we cover major tax incentives:

The US

Qualified Small Business Stock (QSBS) Incentive

The Colorado Advanced Industry Investment Tax Credit (AIITC)

The Georgia Qualified Investor Tax Credit ( the "Angel Tax Credit)

The Illinois Angel Investment Credit Program

The New York State Qualified Emerging Technology Company (QETC) program

Angel Investor Tax Credit (AITC)

Keystone Innovation Zone (KIZ) Tax Credit

Technology and Life Science Economic Development Tax Credit

The UK

Seed Enterprise Investment Scheme (SEIS)

Enterprise Investment Scheme (EIS)

Venture Capital Trusts (VCTs)

Germany

INVEST – Venture Capital Grant

France

Income Tax Reduction for Capital Subscriptions in Unlisted SMEs

Spain

Deduction for investment in new or recently created companies, Spanish Startup Law

Ireland

Employment and Investment Incentive (EII)

Italy

Tax Incentives for Investments in the Share Capital of Innovative Start-ups and Innovative SMEs

The detailed data on the incentives is presented in the full report.

DISCLAIMER: This report analyzes market trends and is not a source of definitive or complete data. Due to the dynamic nature of the market, it's impossible to provide 100% accurate, allencompassing data. Our research is based on the information we have gathered through different public sources, and it may be corrected as new data becomes available. Investing in startups is inherently challenging and carries significant risks. This report should not be construed as investment, tax, or legal advice. We are not making any recommendations. If you are considering starting a business or making venture investments, you should consult with qualified professionals, who can provide personalized and competent advice.

.webp)