Our tax environment review identifies best practices from leading global startup ecosystems for creating a favorable tax environment that supports the growth of startups to scale-up and unicorn levels.

For the review, we have developed a model for assessing the taxation of venture capital investment returns and the taxation at various stages of a startup's development. This model takes into account both tax brackets in different countries and the impact of key tax incentives.

Lower tax burden and tax incentives can help a company build a strong free cash flow, which will improve the financial results and improve the risk-to-return ratio.

In Part-1 of our Review we highlight the rates of key taxes that are significant at different stages of a startup's growth.

In the following parts of the Review, we will focus on the best practices for tax incentives aimed at stimulating venture investments, R&D, and job creation at all stages of a startup's life cycle.

* * * * * * * * * * * *

In recent years, leading startup ecosystems have intensified their competition to attract startups and their efforts to create conditions for the growth of scale-ups, the localization of unicorn companies.

One of the focuses is the availability of venture capital financing. For example, in 2025, the U.S. took significant steps to simplify and stimulate venture capital investments, including:

- raising the Qualified Small Business Stock (QSBS) threshold to $75 million (up from $50 million). This allows to apply 0% capital gains tax rate on investments in companies valued below this amount.

- the U.S. also simplified access for pension funds to finance venture investments.

The European Union is also developing a strategy to stimulate venture investment and support innovation .

We believe that the tax environment is one of the key factors for the growth of available venture funding. Tax rates and incentives directly influence how a startup grows, where it chooses to locate, and investor’s decisions.

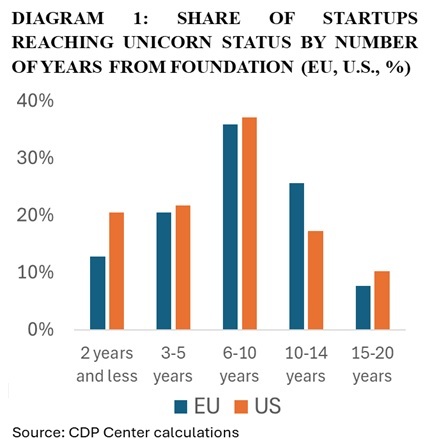

Interestingly, on average, a U.S. startup reaches unicorn status in 7 years from its founding, compared to 7 years and 9 months for a European startup. In both the U.S. and Europe, 36%-37% of startups that become unicorns do so within a 6-10 year timeframe.

Startups that have reached the scale-up stage already possess significant weight and recognition. At this point, they can change their tax jurisdiction to a more favorable one to accelerate future growth and optimize the terms for a future exit.

In our review we focused on the world's leading ecosystems (14 countries and 11 states of the U.S.) that consistently demonstrate strong results in startup exits and the overall development of the ICT and AI sectors.

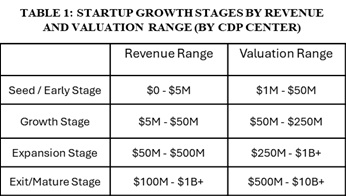

In the model we defined four stages of startup growth, outlining the approximate revenue and valuation ranges for each.

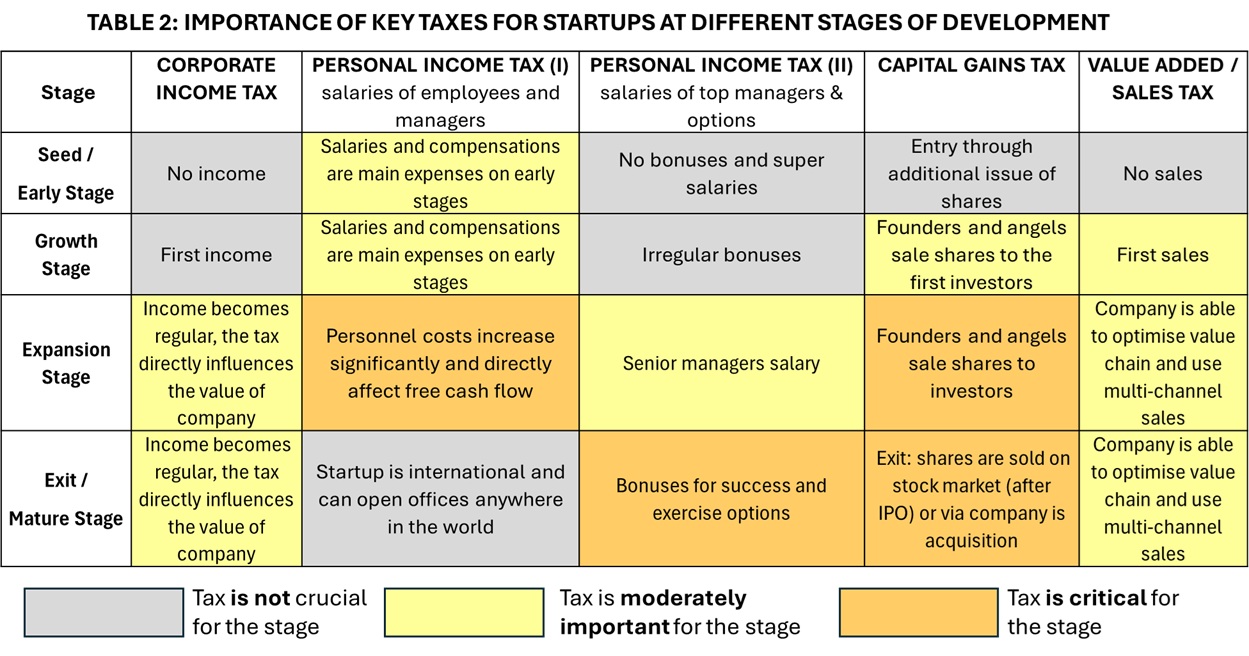

We identified key taxes influencing a startup's investment attractiveness and development. We determined the taxes significance for each growth stage (Table 2).

We consider several key taxes: Capital Gains Tax, Corporate Tax (CIT - Corporate Income Tax), Personal Income Tax (PIT), and Value-added tax (VAT) / Sales tax.

Capital Gains Tax is a tax on the income from the appreciation of a capital investment. It is a key tax for venture investors because, from a financial perspective, their primary goal is the appreciation of their invested capital.

Other taxes also affect a company's financial performance, and thus a startup's investment attractiveness.

We have compiled the tax brackets for the selected taxes across the selected countries and U.S. states, identifying the applicable rates for startups in each. For Personal Income Tax, we also calculated taxes for specific salary categories: PIT I (for annual salaries up to $50,000 and $100,000) and PIT II (for annual salaries of $500,000 and an example options package).

BEST PRACTICES FOR A TAX-FRIENDLY ENVIRONMENT

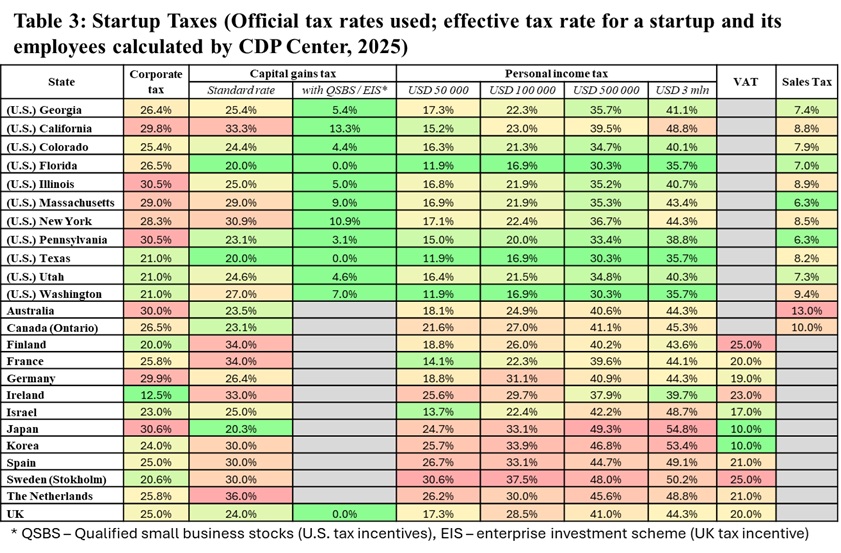

Our analysis of key tax rates at different startup growth stages (Table 3) shows that the most favorable tax environment exists in Texas, Florida, and Washington (state).

Capital Gains Tax: Texas and Florida offer capital gains tax rate at 20% (20% federal, 0% state). Washington state has a 27% rate (20% federal, 7% state). When the federal Qualified Small Business Stock (QSBS) exclusion is applied, the effective tax rate is 0% in Texas and Florida and 7% in Washington state.

Personal Income Tax (PIT): All three states offer the lowest possible personal income tax rates for both average (PIT 1) and high salaries and options (PIT II). This is because all three states have a state PIT of 0%, so only the federal rate (up to 37%) is paid. This is particularly significant for early-stage startups and leading companies as well, as salaries in the ICT and high-tech sectors are higher than the national average in all observed countries.

Corporate Tax: Corporate tax in these ecosystems is 21% in Texas and Washington and 27% in Florida. However, these states have tax incentives stimulating R&D, job creation, and purchasing high-tech equipment, which make the effective rates much lower. We will cover these incentives in future publications.

Sales Tax: Sales tax is 9.4% in Washington, 8.2% in Texas, and 7.0% in Florida. From the scaling stage, as companies enter international markets, the state sales tax plays a decreasing role.

It is also important to highlight the best practices for specific taxes.

Best Practices for Corporate Tax

Corporate tax does not affect a startup until the company begins generating income. It becomes a systemic factor during the Expansion Stage and as the company prepares for an IPO or acquisition. In most of the countries and states we analyzed corporate tax rates range is between 25% and 30%. Ireland has the lowest rate at 12.5%, while Finland and Sweden have rates of 20% and 20.6%, respectively.

In most of the ecosystems studied, there are a corporate tax incentives (tax relief, tax credit etc.) related to stimulating R&D activities. In the U.S., almost all analysed states also have incentives linked to job creation.

Furthermore, in some ecosystems, a zero rate for corporate tax is offered in the early stages of a startup's formation.

An overview of tax incentives for R&D and jobs creations that can reduce corporate tax will be presented in the next parts of the review.

Best Practices for Personal Income Tax

Personal Income Tax (I) is the personal income tax rate on employees and management compensation, specifically for annual salary up to $50K and $100K. This tax is a significant expense in a company's early stages, but becomes most critical during the Expansion Stage when the company expands its staff to serve a developing market.

At the Exit / Mature Stage, as startups go international and open offices in various countries, the importance of the PIT I rate on salaries at the headquarters decreases.

Overall, the personal income tax rate for these salary levels is lowest in America (11.9%–18% for a $50K salary; 16.9%–24% for a $100K salary) and in a few European countries, including France (14.1% and 22.3%, respectively) and the United Kingdom (17.3% and 28.5%). We calculated this tax for a typical startup employee not eligible for extra deductions. It is worth noting that some European countries, like Germany, have a system of deductions that significantly lowers tax rates in some cases (e.g., family, children).

Personal Income Tax (II) is the tax rate on top management salaries and stock options for key employees. (For our model, we used for annual salaries and options up to $500K and $3M.) This tax rate becomes significant during the Expansion Stage, when top managers begin receiving high salaries. Its importance increases during the Exit/Mature Stage, when management receives significant bonuses and begins to realize their stock options.

Texas, Florida, and Washington show the lowest tax rates for this income category (30.3% on $500K and 35.7% on $3M), while Ireland's rates are 37.9% and 39.7% respectively.

Best Practices for Capital Gains Tax (CGT)

Capital Gains Tax is a direct tax on the returns from entrepreneurship and investment, incurred when startup shares are sold—typically during the Expansion Stage and Exit / Mature Stage.

In most analysed countries and states, the CGT rate ranges from 20% to 30%. The lowest rates are in Texas, Florida, Washington (state), and Japan (20%). However, the effective rate in the U.S. is often much lower due to the Qualified Small Business Stock (QSBS) provision, which provides a 0% tax rate on capital gains for investments in companies valued below $75M (previously $50M).

The UK has a similar measure with its Enterprise Investment Scheme, which offers a 0% CGT rate on a maximum annual investment of up to £1M (~$1.35M). Australia, Canada, and Ireland also have CGT measures, though they are limited by investment amount. We will examine these measures in detail in the next parts of the review.

Other Taxes

The Value Added Tax (VAT) / Sales Tax (in the U.S., Canada, and Australia) affects startup financial results.

For startups in the early stages of growth, these taxes are difficult to administer. On the later stages the impact of these taxes diminishes as companies optimize their value chains and use multi-channel sales.

Also, we did not include employee social security contributions in our model (the tax rate across the analyses ecosystems varies from 1.5% to 15%), because these payments are directly tied to the standard of living and social benefits. Our analysis shows that businesses often have significant opportunities for deductions (e.g., through providing private insurance) or receive additional incentives specifically for the ICT and R&D sectors.

* * * * * * * * * *

DISCLAIMER: The project team did not aim to provide a detailed description of tax regulations or mechanisms for calculating effective tax rates for specific companies, taking tax incentives into account. Since the taxation system of each country and each city is complex and the situation for all companies is individual, this review doesn’t contain any taxation or incentives solutions and doesn’t make any recommendations. In case you are planning to do startup business or make venture investments you should contact taxation consultants, who may provide you competent advice.

#startup #venture #ecosystem #taxation #investments #ICT #AI #artificialintelegence

.webp)