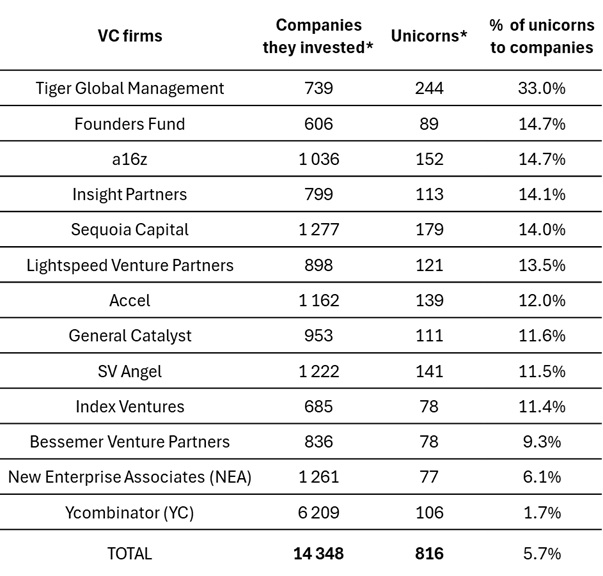

Our report covers trends in 14 categories (AI Infrastructure, App & Software Development, Crypto, Data analytics, EdTech, Enterprise, ESG, Fintech, Health / Bio Tech, Industries, Legal, Media & Advertisement, Science & Research, Services & Retail) and database of startups backed by leading 13 venture capital firms (a16z - Andreessen Horowitz, Sequoia Capita, YC - YCombinator, Index Ventures, Founders Fund, Bessemer Venture Partners, Insight Partners, Accel, Lightspeed Venture Partners, General Catalyst, New Enterprise Associates (NEA), Tiger Global Management, SV Angel).

This report is designed to help companies, investors, and founders track the trends and benchmarks established by venture capital leaders.

Updated monthly, our report and database provide verified data and expert insights.

We examine the activities of the largest and most experienced firms — the technologies and sectors they support, and the types of investments they make. We believe that a deeper understanding of the priorities held by venture capital market leaders can help our subscribers more effectively build their investment and growth strategies.

The VC companies we analyze are smart money – they backed more than 800 companies, which became unicorns or even decacorns.

According to our calculations, because of their role in the ecosystem and their smart approach, the leaders reach almost around 15% unicorns to their portfolio.

Key facts (February 2026)

158 deals (4.9% from February total 2026 deals)

114 deals from 158 were leaded by this 13 venture firms, in other 45 deals, the firms participated in syndicates.

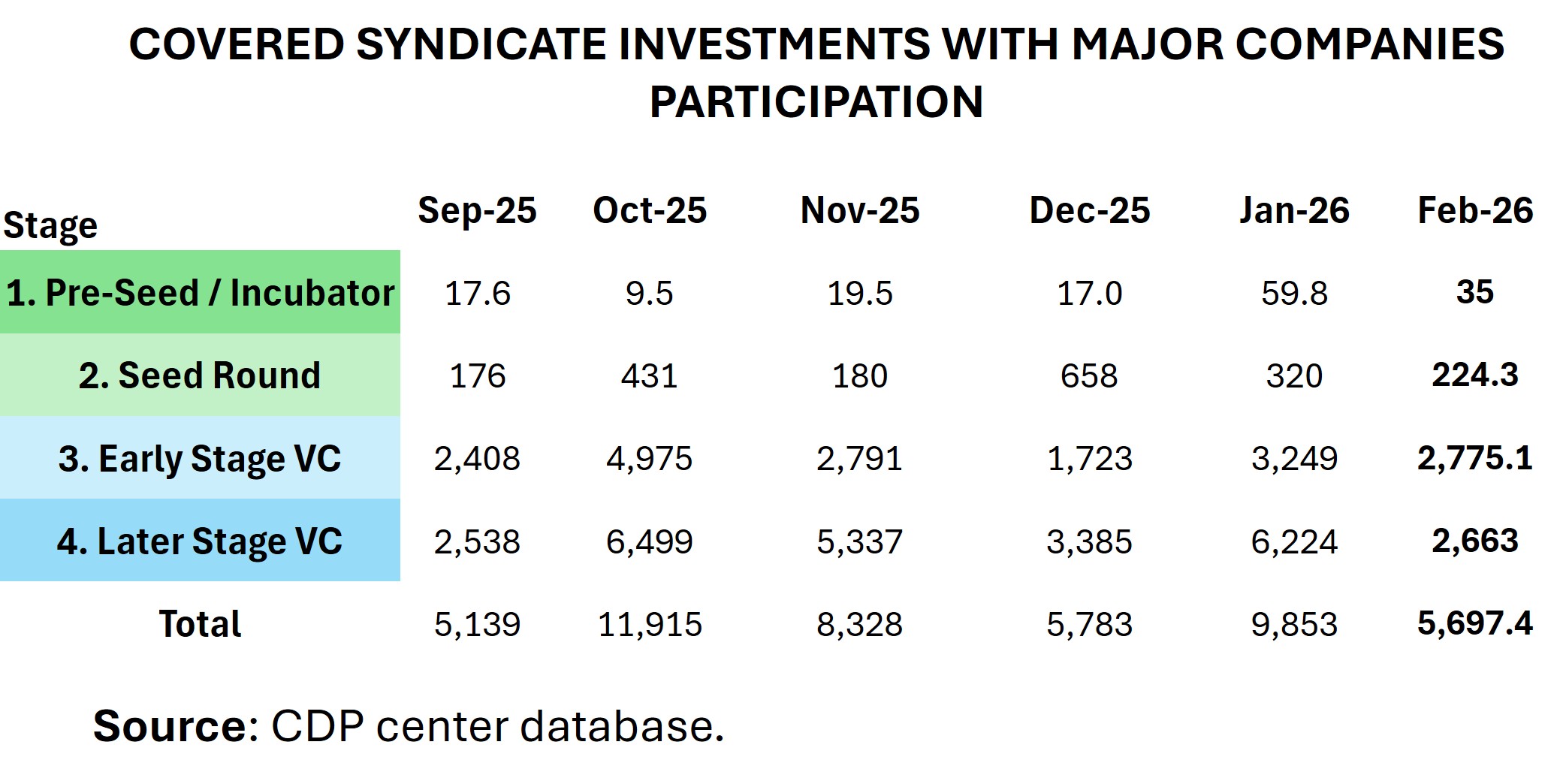

Syndicates with top VC included USD 5.7 bn (not including megadeals)

Top VC supported 12 of February unicorns (54.5% from 22 unicorns according to Dealroom Unicorns)

The report based on 158 deals concluded or announced with the participation of these companies in February 2026— approximately 4.9% of the total number of venture investments for the month. 114 deals from 158 were leaded by this 13 venture firms, in other 44 deals, the firms participated in syndicates.

In February 2026, the top venture funds backed 44.3% of Pre-Seed / Incubator stage rounds and 12% of Seed stage rounds.

The total share of VC backed by top firms: Pre-Seed, Incubator, and Seed rounds backed by major VC firms is 56%, which is average compared to previous months.

The largest proportions of Pre-Seed and Seed rounds were observed in Legal (100%, 6 total), AI Infrastructure (72%), App & Software development (65%).

The data on the number of deals (Rounds) continues to show a level below last year February (-19% compared to February 2026 with 4,304 deals versus 3,480 and -33% compared to February 2024).

The share of new Pre-Seed / Seed rounds has declined to 27-28%, one of the lowest levels in recent years. Still the last months are a little higher than annual average: January 2026 – 30.4%, February 2026 - 35.6%.

Almost all new startups supported by market leaders are implementing or using AI. This represents a very high barrier to entry and places high demands on the team.

AI integration has become virtually mandatory for startups. As of March 2026, 100% of Pre-Seed startups & 100% of Seed-stage startups either use or have announced the use of AI in their products.

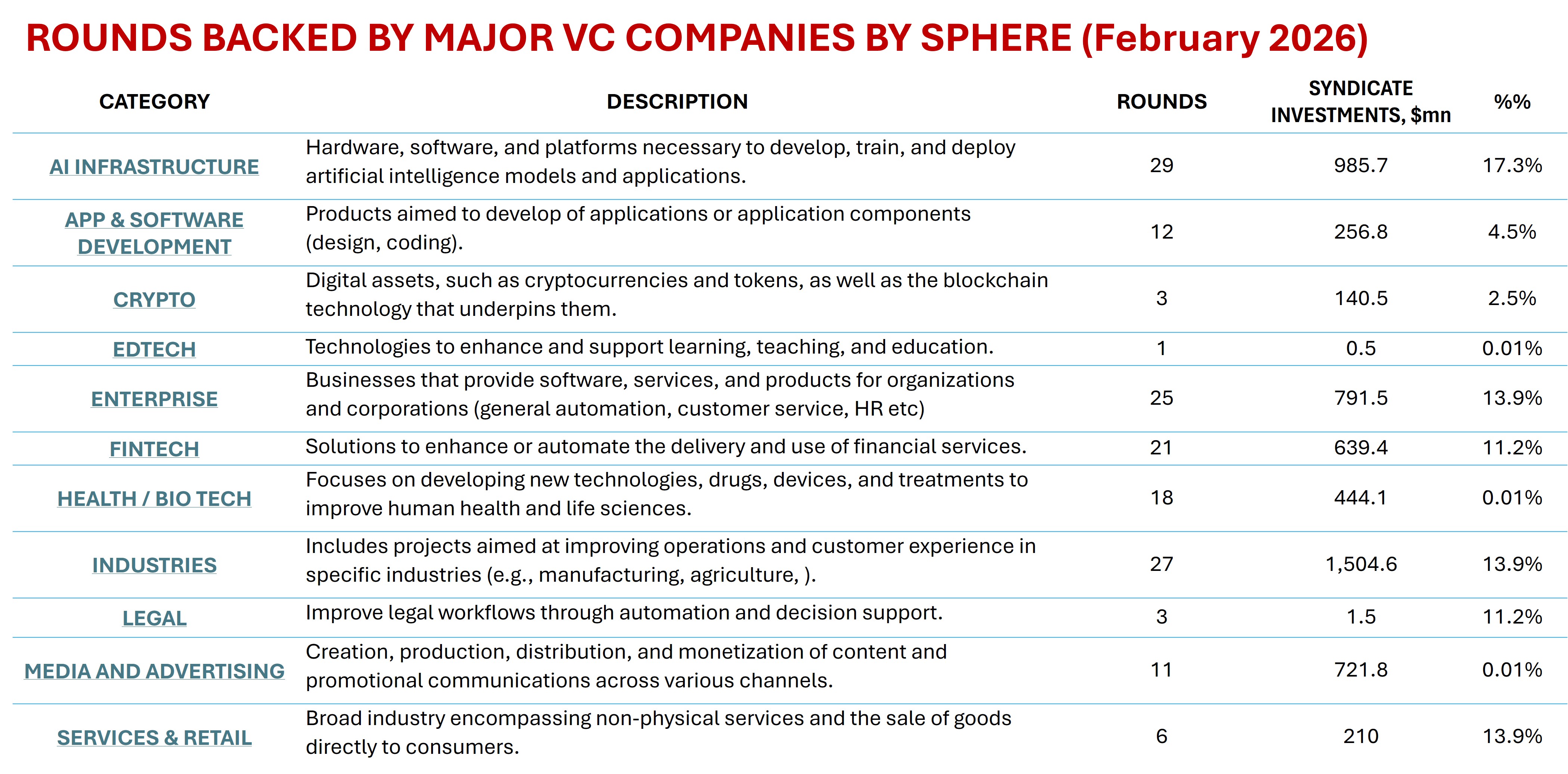

PART 2. ANALYTICS BY SPHERES

2.1. AI Infrastructure

This category includes startups developing the hardware, software, and platforms necessary to develop, train, and deploy artificial intelligence models and applications.

In February 2026, among top VC funds, the AI Infrastructure industry accounted for 17.4% of investments in terms of volume (USD 986 ml out of USD 5.6 bn) and 18.5% of deals (29 out of 157). At the same time, the sector is one of the most rapidly developing—we classified 18 out of 29 deals (62%) as Pre-Seed / Incubator, which shows that the industry is considered one of the most attractive.

Also in February, the industry saw two new unicorns: Render (syndicate lead: Georgian; among participants: Bessemer Venture Partners, General Catalyst) with a valuation of USD 1.4 billion, and Ayar Labs (syndicate leads: Nvidia, AMD; among participants: Insight Partners, Sequoia Capital) at USD 3.8 billion.

We have identified the following groups within AI Infrastructure:

• AI Development & Agent Frameworks – 15 startups (USD 319 million)

• AI Gadgets – 1 startup (USD <1 million)

• Applied, Interactive & Research AI – 6 startups (USD 120.5 million)

• Compute & Systems Optimization – 2 startups (USD 500.5 million)

• Data & Knowledge Infrastructure – 5 startups (USD 45 million)

2.1.1. AI Development & Agent Frameworks

This subcategory includes startups developing software and applications aimed at the development, deployment, and monitoring of AI models and agents, including their stability and permission systems. This category includes 15 startups with a total venture funding volume of USD 319 million.

Among the Pre-Seed stage, we found YC-backed Carrot Labs and Sponge to be the most interesting.

• Carrot Labs (link) is developing continuous-learning AI models for enterprises. The team's premise is that companies can create their own foundation models tailored to their specific tasks and workflows. Furthermore, these models should self-develop and optimize by taking into account their performance results and the company's efficiency metrics.

• Sponge (link) is creating financial infrastructure to enable transactions between businesses and AI agents. Using these protocols and infrastructure, AI agents will be able to autonomously make purchases from real businesses and even participate in financial transactions.

As many as three projects are developing AI agents designed to create, support, and develop other AI agents:

• Portkey - Providing AI developer teams with the tools they need for production: AI Gateway, Observability, Guardrails, Governance, and Prompt Management. (USD 15 million. Syndicate lead: Elevation Capital; among participants: Light Speed Venture, link).

• Union - A unified AI development platform that streamlines the complex operations required to develop, deploy, and manage AI, ML, and agents. (USD 38.1 million. Syndicate lead: NEA, link).

• Braintrust - AI agents to help organizations efficiently test, monitor, and deploy reliable AI applications. (USD 80 million. Syndicate lead: ICONIQ; among participants: a16z, link).

Among later-stage startups:

• Encord (link) - The platform provides a data infrastructure to streamline the training data lifecycle for corporate AI models via automated data labeling, curation, post-training alignment, data management, and orchestration. (USD 60 million. Syndicate lead: Wellington Management; among syndicate participants: YC).

• Render (link) reached unicorn status after raising USD 100 million (valuation: USD 1.4 billion). The platform is developing a cloud hosting platform for deploying apps and AI agents with zero ops costs and seamless scaling.

2.1.2. AI Gadgets

This month, we would like to highlight one startup: Button Computer (YC backed, link). They develop a wearable AI assistant that answers user questions when a button is pressed. It appears to be a highly convenient and effective gadget.

2.1.3. Applied, Interactive & Research AI

This group includes projects aimed at developing or upgrading AI models or approaches to their creation.

• Confluence Labs (YC backed, Pre-Seed, link) is already developing foundation models optimized for learning on limited data. The project notes that [????]. The startup estimates that its ARC-AGI-2 benchmark reaches 97.9% at a cost of ~USD 12, vastly outperforming other available models in quality.

• BeyondMath (USD 18 million investment. Syndicate lead: Cambridge Innovation Capital; among participants: Insight Partners, link) is creating specialized physics-informed neural networks to accelerate complex multiphysics simulations: engineering, critical tasks, aerospace, automotive, etc.

• Simile (USD 100 million. Syndicate lead: Index Ventures, link) is creating a simulation platform that uses generative agents to model human behavior and predict real-world decision-making.

2.1.4. Compute & Systems Optimization

This group includes hardware and algorithms specifically aimed at accelerating the performance of core AI or its applications.

Both projects backed in February (Piris Labs, backed by YC; Ayar Labs, backed by Nvidia and AMD, including Insight Partners and Sequoia Capital) were startups in the field of applied optical data transmission technologies.

• Piris Labs (link) is developing optical technologies to speed up communication data processing and remove bottlenecks.

• Ayar Labs (link), which became a unicorn, is the developer of optical engines to replace copper interconnects and build compute nodes that function as a single, giant GPU, improving AI hardware efficiency.

2.1.5. Data & Knowledge Infrastructure

This group includes infrastructure aimed at creating new datasets for model training or improving the stability and security of model operations through new tech solutions.

• Asimov (backed by YC, link) is tracking real-world human movement data for businesses and households.

• One Robot (backed by YC, link) is creating pre-trained models for robot evaluation and training.

• Deeptune (USD 43 million investment with a16z participation, link) is creating a new approach for AI training. The startup is building a simulation environment—including problems, datasets, and infrastructure—where AI can practice executing tasks. This allows for both evaluating the results of the AI model and further training it on pre-set tasks.

2.2. App & Software Development

This group supports the development of applications or application components (design, coding). In February, top VCs funded 12 startups with USD 256 million in investments.

• SolveAI (backed by Accel, Google Ventures, USD 50 million, link) is a conversation-to-software platform that allows users to build custom, enterprise-grade applications through simple chat. A standout feature of the program is that it focuses not just on coding, but on recognizing problems and generating solutions to those problems using applications.

• A similar direction is being developed by Canary (backed by YC, link), which is creating a thinking AI that "understands" code, automating pull request analysis, testing, and merging.

• In February, Code Metal became a software development unicorn (syndicate led by Salesforce Ventures with Accel participation, USD 250 million, valuation USD 1.25 billion, link)—a platform for verifiable code translation, converting high-level code into optimized, low-level hardware languages.

We particularly liked two startups that are taking new steps in working with code:

• Glue (backed by YC, link) is opening a new frontier in code development and integration with design solutions. Specifically, the company is creating a design that enables AI agents to use design canvases.

• Emdash (backed by YC, link) also offers a new development environment enabling parallel coding by AI agents.

Another startup is creating better conditions for code developers:

• Modem (syndicate led by Accel, USD 4.4 million, link) ingests unstructured feedback from channels like Slack, Discord, and email—such as recurring bugs or feature requests—and translates them into highly contextualized tasks.

If you are interested in information about venture industry insights and current funding trends, subscribe to our monthly reports here: venture.cdp.center

Each report covers trends in 14 categories (AI Infrastructure, App & Software Development, Crypto, Data analytics, EdTech, Enterprise, ESG, Fintech, Health / Bio Tech, Industries, Legal, Media & Advertisement, Science & Research, Services & Retail) and database of startups backed by leading 13 venture capital firms(a16z - Andreessen Horowitz, Sequoia Capita, YC - YCombinator, Index Ventures, Founders Fund, Bessemer Venture Partners, Insight Partners, Accel, Lightspeed Venture Partners, General Catalyst, New Enterprise Associates (NEA), Tiger Global Management, SV Angel)

The detailed data on the rounds is presented in the full report.

DISCLAIMER: This report analyzes market trends and is not a source of definitive or complete data. Due to the dynamic nature of the market, it's impossible to provide 100% accurate, allencompassing data. Our research is based on the information we have gathered through different public sources, and it may be corrected as new data becomes available. Investing in startups is inherently challenging and carries significant risks. This report should not be construed as investment, tax, or legal advice. We are not making any recommendations. If you are considering starting a business or making venture investments, you should consult with qualified professionals, who can provide personalized and competent advice.

.webp)